ITR-1 vs ITR-2 – Which Form Should You File? (2026 Guide)

ITR-1 vs ITR-2 – Why Choosing the Right Form Matters

During every income tax season in India, one of the most common questions taxpayers ask is: “Should I file ITR-1 or ITR-2?”

Both forms are designed for individuals, but they apply to different types of income and taxpayers. Understanding the difference between ITR-1 vs ITR-2 is essential because filing the wrong income tax return form can result in a defective return notice under Section 139(9), delayed refund processing, or even additional compliance issues.

Many taxpayers mistakenly assume that if they are salaried employees, they should always file ITR-1 (Sahaj). However, this is not always correct. If you have capital gains from shares, multiple house properties, foreign assets, or other complex income sources, ITR-2 may be required instead.

In recent years, the Income Tax Department has significantly strengthened verification systems. With tools like AIS (Annual Information Statement), TDS records, and high-value transaction reporting, the department now cross-checks income data more efficiently. Any mismatch between your declared income and official records may trigger scrutiny.

That is why selecting the correct ITR form before filing your return is extremely important.

If you are new to income tax filing, you can first understand the basics by reading this guide on What is ITR:

https://www.sscoindia.com/blog/what-is-itr-income-tax-return-india-2026-guide

You can also explore a detailed explanation of Types of ITR Forms Explained to understand how different return forms apply to different taxpayers.

This guide will help you clearly understand the difference between ITR-1 and ITR-2, their eligibility criteria, and how to choose the correct form for your income tax return in 2026.

What is ITR-1 (Sahaj)?

One of the most widely used income tax return forms in India is ITR-1, also known as Sahaj.

The form is specifically designed for individuals with simple income structures, primarily salaried taxpayers. Because of its simplified format, it is commonly used by employees who earn income mainly through salary and basic investments.

ITR-1 Eligibility

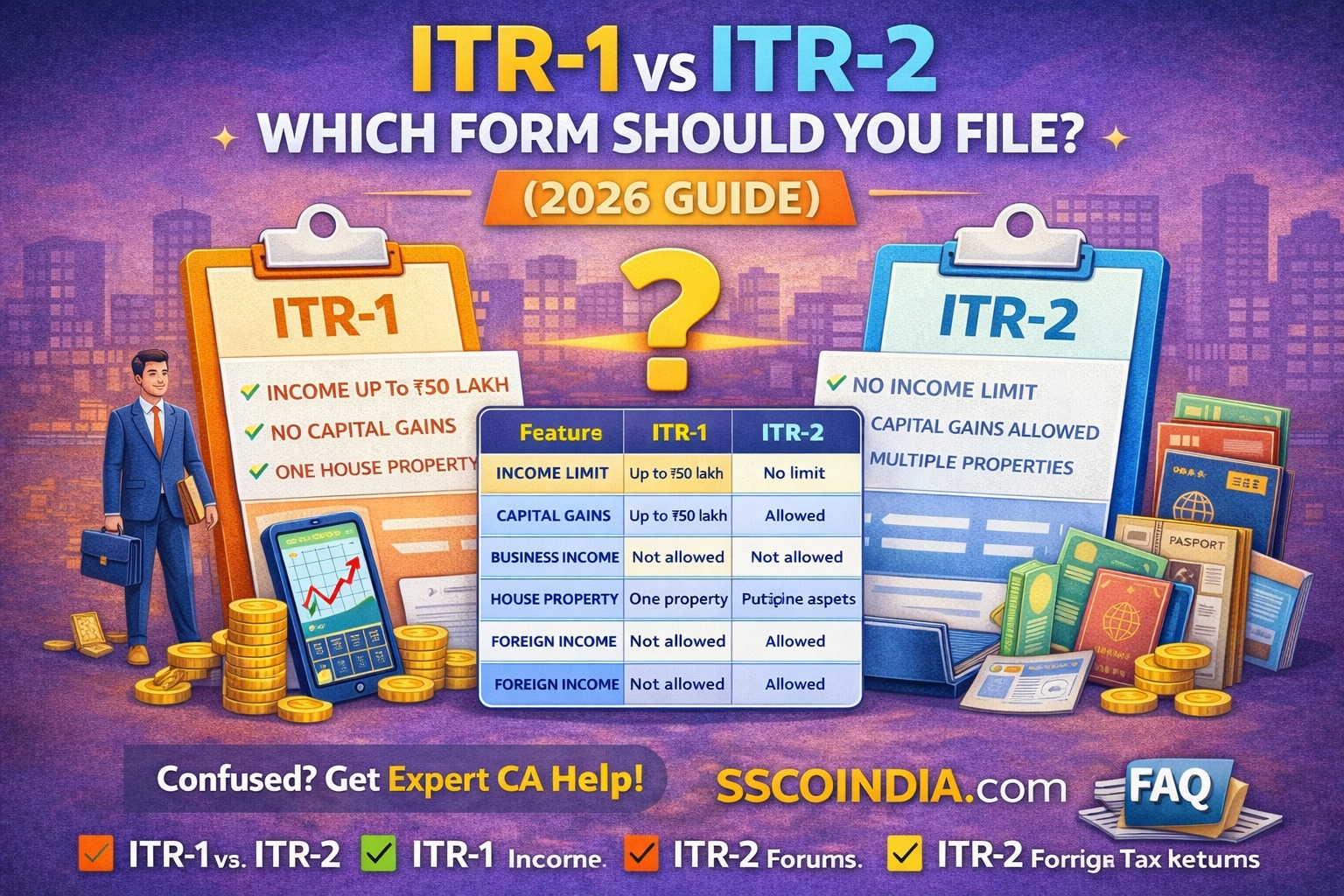

The ITR-1 eligibility criteria are fairly straightforward. This form can be used by resident individuals whose total income does not exceed ₹50 lakh during the financial year.

Who Uses ITR-1?

ITR-1 is generally used by:

-

Salaried employees

-

Pensioners

-

Individuals earning income from one house property

-

Individuals earning interest income from savings accounts or fixed deposits

For example, if you are a salaried employee earning ₹12 lakh annually, living in a self-occupied house, and earning interest from a savings account, ITR-1 for salaried employees is the appropriate form.

However, ITR-1 is designed only for simple tax situations. If your financial profile becomes more complex, you may need to use a different return form.

Understanding these eligibility conditions helps taxpayers avoid filing errors and ensures smoother income tax return processing.

Who Can File ITR-1?

To determine whether you should file ITR-1, you must first check whether your income sources fall within the permitted categories.

The following taxpayers are typically eligible to file ITR-1 (Sahaj).

✔ Salaried individuals earning income from employment.

✔ Individuals receiving pension income from previous employment.

✔ Individuals earning income from one house property.

✔ Individuals earning interest income from bank deposits or other sources.

✔ Individuals with agricultural income up to ₹5,000.

For example, consider a salaried employee working in a private company who earns ₹15 lakh annually and receives interest from a savings account and fixed deposits. If the individual owns only one house property and does not have capital gains, ITR-1 is the correct form.

Similarly, a retired pensioner earning pension income and bank interest can also file ITR-1.

However, once additional income sources such as stock market gains, multiple properties, or foreign income come into the picture, ITR-1 eligibility no longer applies.

This is where many taxpayers make mistakes.

Who Cannot File ITR-1?

Understanding who cannot file ITR-1 is just as important as knowing who can.

Many taxpayers unknowingly file ITR-1 even when they are not eligible. This is one of the most common reasons for defective return notices from the Income Tax Department.

You cannot file ITR-1 if you have any of the following income sources:

Capital Gains from Shares or Property

If you have earned profits from:

-

Selling shares

-

Mutual funds

-

Property transactions

you must file ITR-2 instead of ITR-1.

More Than One House Property

Individuals owning multiple residential properties must report that income using ITR-2.

Business or Professional Income

If you are a freelancer, consultant, or business owner earning professional income, ITR-3 or ITR-4 may apply instead.

Foreign Assets or Foreign Income

If you hold foreign investments or earn income from overseas sources, ITR-1 cannot be used.

Director in a Company

Individuals serving as directors in a company must use ITR-2 even if their income is primarily salary.

These restrictions often create confusion among taxpayers, which is why choosing the correct form is essential before filing the return.

What is ITR-2?

While ITR-1 is meant for simple income structures, ITR-2 is designed for individuals with more complex financial situations.

The ITR-2 eligibility applies to individuals and Hindu Undivided Families (HUFs) who do not have business income but have other types of income beyond basic salary.

ITR-2 for Capital Gains

One of the most common reasons for filing ITR-2 is capital gains.

If you have sold:

-

Shares

-

Mutual funds

-

Property

-

Bonds or securities

you must file ITR-2.

Income Covered Under ITR-2

ITR-2 includes taxpayers with income from:

-

Capital gains

-

Multiple house properties

-

Foreign income or assets

-

High-value investments

For example, if a salaried employee also trades in the stock market or sells property during the year, ITR-2 becomes mandatory.

Because of the additional reporting requirements, ITR-2 is more detailed than ITR-1.

Who Should File ITR-2?

The following taxpayers typically need to file ITR-2.

✔ Individuals earning capital gains from shares or mutual funds

✔ Individuals owning more than one house property

✔ Individuals holding foreign assets or foreign income

✔ Individuals serving as directors of companies

✔ High-income individuals with complex investment portfolios

For instance, if a salaried professional earns ₹18 lakh annually and also sells mutual funds during the financial year, ITR-2 must be filed because capital gains are involved.

Similarly, individuals who own two rental properties must report this using ITR-2.

Because income structures are becoming more complex due to investments and global income sources, many taxpayers today fall under ITR-2 eligibility.

If you are unsure which form applies to your situation, professional guidance can prevent mistakes.

For accurate and stress-free income tax return filing in India, consider taking expert assistance from SSCOIndia. Their experienced tax professionals help individuals choose the correct ITR form, avoid defective returns, and ensure timely filing across India.